Skip to content

Media

Careers

Subscribe

Media

Careers

Subscribe

Client Portal

Contact

Client Portal

Contact

What We Do

Investment Management

Financial Planning

Our Story

The Team

In the Community

In the Media

BFIC Traveling Hat

Market Insights

Resources

Quarterly Newsletters

Quarterly Reports

BFIC Videos

Roads to Retirement

Investing from A to Z

What We Do

Investment Management

Financial Planning

Our Story

The Team

In the Community

In the Media

BFIC Traveling Hat

Market Insights

Resources

Quarterly Newsletters

Quarterly Reports

BFIC Videos

Roads to Retirement

Investing from A to Z

Search

Search

Close this search box.

Weekly TGIF

Another Rapid Rundown

April 26, 2024

Continue Reading »

That 70’s Show

April 19, 2024

Continue Reading »

Nagging Inflation – You Want Fries with That?

April 12, 2024

Continue Reading »

Spring 2024 Newsletter

April 5, 2024

Continue Reading »

TGI-Good Friday: Hot Chocolate

March 28, 2024

Continue Reading »

March Madness

March 22, 2024

Continue Reading »

All About AI

March 15, 2024

Continue Reading »

The State of America – Soft Landing, Hard Politicking

March 8, 2024

Continue Reading »

Amazon Joins the Dow

March 1, 2024

Continue Reading »

Nvidia Saved the Rally

February 23, 2024

Continue Reading »

Undersea & Outer Space – Risk & Reward

February 16, 2024

Continue Reading »

Super Bowl Sunday Sin City Style

February 9, 2024

Continue Reading »

Another Rapid Rundown

February 2, 2024

Continue Reading »

Who Motivates the Motivator?

January 26, 2024

Continue Reading »

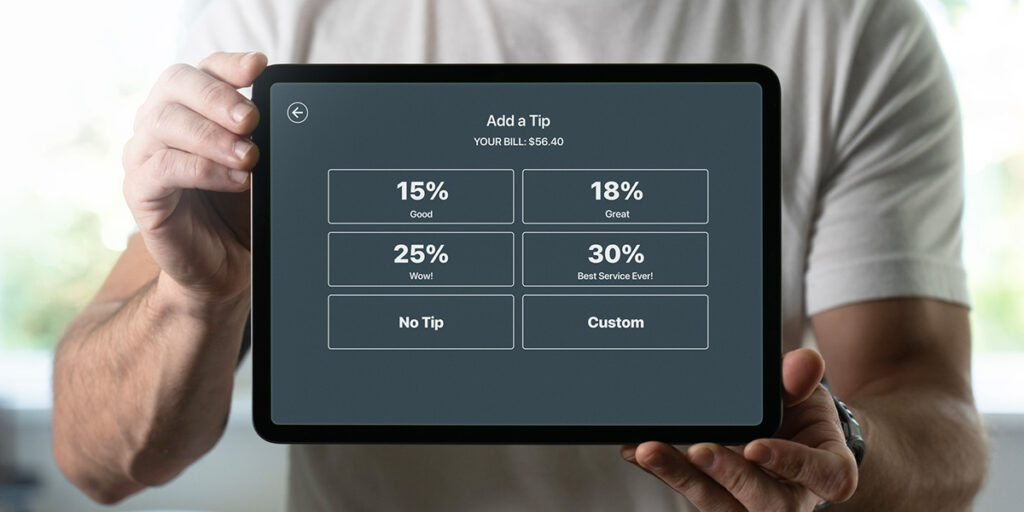

Consumer Takeaway – Too Much Tipping!

January 19, 2024

Continue Reading »

Tomorrow’s Tech Toys Today

January 12, 2024

Continue Reading »

Winter 2024 Newsletter

January 5, 2024

Continue Reading »

Happy New Year!

December 29, 2023

Continue Reading »

Load More

What We Do

Investment Management

Financial Planning

Investment Management

Financial Planning

Our Story

The Team

In the Community

In the Media

BFIC Traveling Hat

The Team

In the Community

In the Media

BFIC Traveling Hat

Resources

Market Insights

Quarterly Newsletters

Quarterly Reports

BFIC Videos

Roads to Retirement

Investing from A to Z

Market Insights

Quarterly Newsletters

Quarterly Reports

BFIC Videos

Roads to Retirement

Investing from A to Z

Contact

Contact Us

Client Portal

Careers

Contact Us

Client Portal

Careers

Facebook-f

Linkedin-in

Instagram

Youtube

Search

Search

Subscribe to Our Newsletter

And receive our free “Investing From A to Z” ebook.

First Name

Last Name

Email Address

Subscribe